Tencent 3q2023

Like the previous quarter, Tencent continued its shift towards higher profitability products/services. Market valuation appears cheap and the management focused on buy-back.

Summary of results

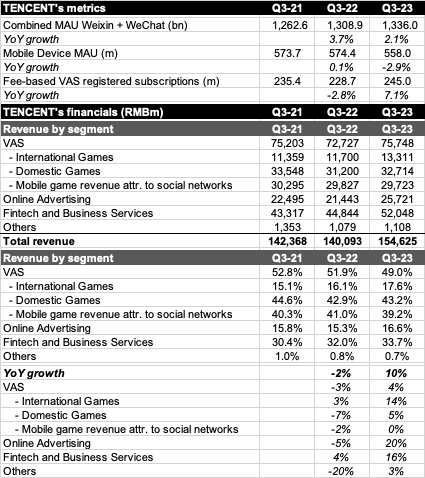

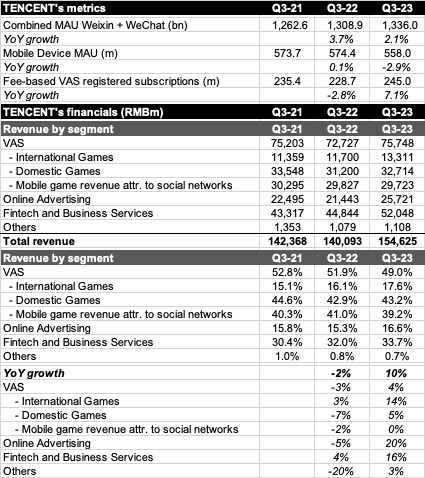

In 3q2023 revenue increased by 10% mostly due to expansion of on-line advertising (+20%) and FBS (+16%) while VAS (Gaming and Social Networks) continued solid 4% growth led by International Games.

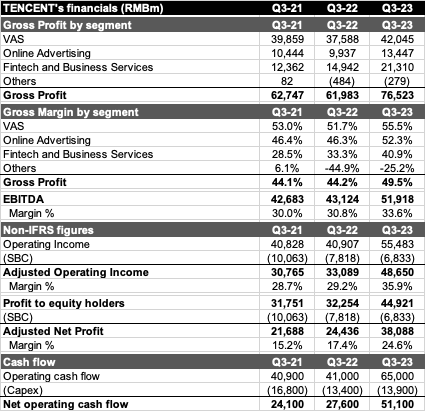

Company's Gross Margin jumped from 44% (2021-22) to the current 49.5% with reported improvements spread across all the different reporting units (FBS from 28% to nearly 41%).

Outstanding cash flow in 3q2023 (RMB51bn) compared to RMB27.6bn in 2022).

As at September 2023, net cash position totalled RMB36.4bn. Fair value of shareholdings in listed investee companies totalled RMB464.4bn (USD64.7bn) and the carrying book value of unlisted investments was RMB347.2bn (USD48.4bn).

During the third quarter, the Company repurchased approximately 47.5m shares on the Hong Kong Stock Exchange (consideration of approximately RMB14.0bn).

Remarks from the CC

On Mini Programs and Mini Games: (i) Each day, several 100 million unique user visits and interact with over 1 million unique Mini Programs, (ii) Mini Games, which is a successful vertical use case for Mini Programs, has become the largest casual game community in China. We monetise these open platforms primarily through payment take rates and a very light advertising load resulting.

... We believe we have moved into a high-quality revenue growth model. Under this model, we can now deliver greater operating leverage than in the past. Prior to 2021, our gross and operating profit typically grew at similar or slower rates versus our revenue. While in 2021 and '22, slowing revenue growth translated into even slower profit growth or in some certain quarters, profit declines. However, entering 2023, solid revenue growth rates have translated into substantially faster growth and operating profit growth rates...

So we believe that the current level of margin -- of gross margin is sustainable, and we believe that there is room for margins to improve further. If you look at the advertising segment, for example, the gross margin has improved from 30% to around 50%. Our closest global comparable is running an advertising gross margin of 18%.

Capital allocation:

... We do have a very strong cash flow alongside with a very large investment portfolio, half of which is actually in liquid stocks. So we do have the flexibility of using different tools to increase shareholder return...

... at this point in time, if you look at the market, the valuation in the market for China in net stock is almost at historical lows, right? So I would say, at this point, buyback will be a more favourable means for our shareholders than other means ...

... given what we view as our share price dislocation, our primary use of cash has been buying back our own shares.

Valuation

At the current market price, capitalisation is nearly HKD3tn. Fair value of investments amount to HKD800bn. LTM Adjusted Operating Income was HKD186bn with the the multiple setting close to 12x.